Profit from Patience: How to Identify Companies Worth Holding for Decades

Profit from Patience: How to Identify Companies Worth Holding for Decades

I was reading my five-year-old investment journal the other day.

You know what surprised me?

The top-performing investments were not the smart buy and sell ones.

They were the good businesses I simply bought and waited, and let time work its magic.

This got me thinking.

The investing wealth we're all dreaming about don't usually come from purchasing the next fad stock or exactly the timing of the market activity.

They are a byproduct of discovering great businesses and the vehicle to survive all of the whipsawing of the market.

I'm just starting my investment years, but I've been reading about the greats obsessively. And there's something that just keeps jumping out at me:

The average investor holds a stock for a mere 10 months.

But the real investors who are actually creating real wealth? They are thinking in terms of decades, not days.

This disconnect isn't just interesting – it's where our potential awaits.

I want to introduce the five core traits I've identified in companies worth holding for decades. I've been studying this aggressively, looking at both the numbers and the qualitative details that separate short-term winners from genuine long-term compounders.

The Hidden Power of Patience

Let me show you something that took my breath away when I first came across it:

$10,000 in Microsoft at its IPO would currently be worth around $1.5 million

$10,000 in Amazon at its IPO would have grown to about $200,000

$10,000 in Google when it went public would now be worth nearly $33,000

These are not anecdotal cherry-picks. These are what happen when you discover wonderful businesses early and simply. hang in there.

However, here's the one thing that I've learned which surprised me: research shows that perhaps 80% of market returns are derived from only 20% of trading days.

More surprising? Omitting just the 10 best days during a 30-year period can halve your returns.

This is why I've become convinced that trying to time the market is so dangerous – you're almost guaranteed to miss some of the most important days.

I used to think that succeeding at investing was all about finding the next big thing.

Now I realize that it's about developing the right mindset. Patience to stay the course through times of volatility. Discipline to stay immune to noise.

I'm still learning this myself. It hurts to watch a stock you own fall 30% during market panic. But I've learned that's exactly when conviction is critical.

Characteristic #1: Durable Competitive Moats

The first thing I look for in a potential decade-hold is a good competitive moat.

I used to believe that a moat was simply the biggest company in an industry. But by studying companies such as Microsoft, I have realized it's more than that.

A moat is what protects a company's profit from the competition that would dearly love to get in there and steal market share by undercutting them.

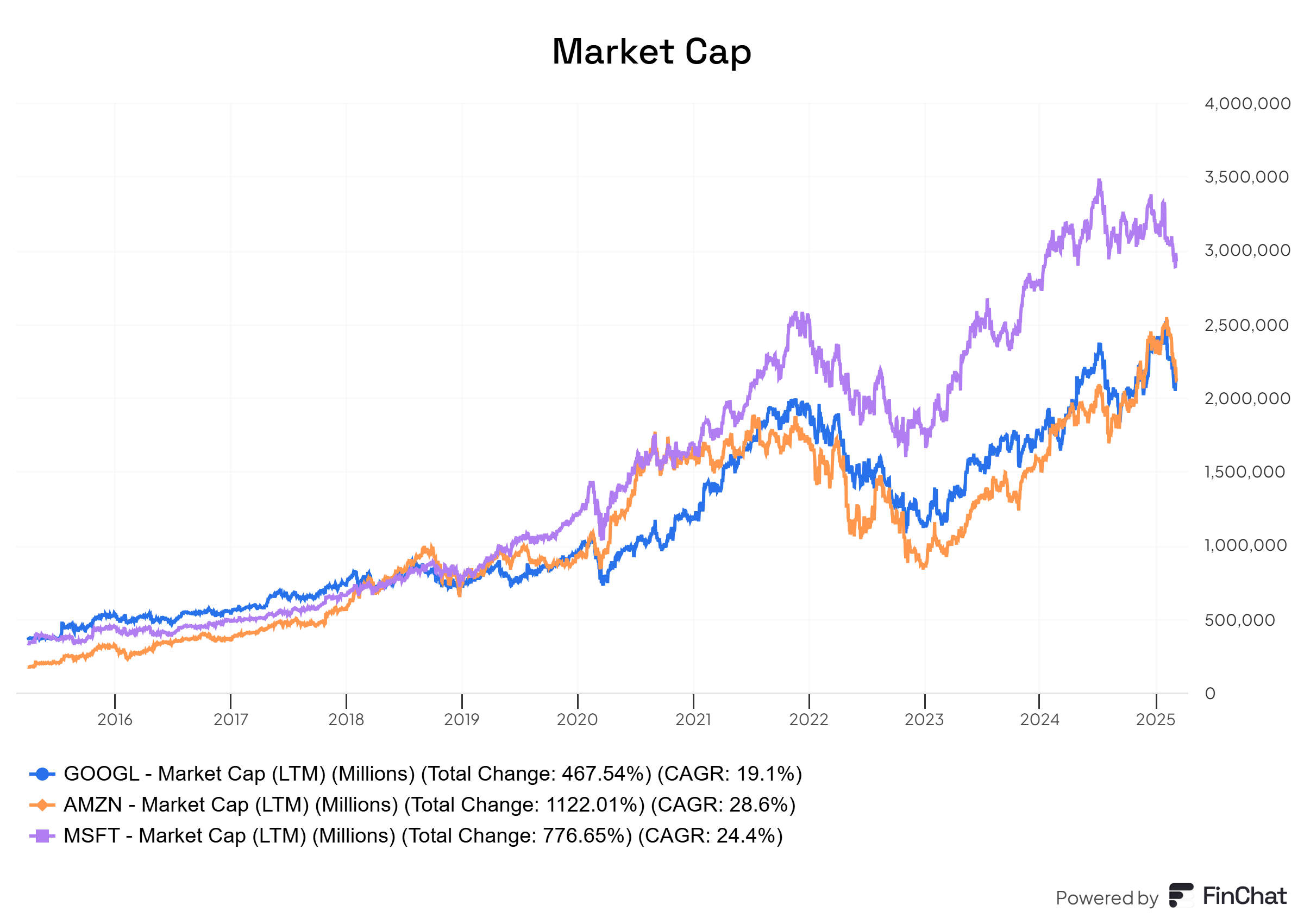

Let's take Microsoft, for instance. Back when I started following the company, everyone thought they were past their best days. But check out what's happened to their operating margins:

Their operating margin has increased from 25% in 2010 to 43% in 2025. That's not just impressive – it shows that their competitive position is strengthening, not weakening.

From what I have learned, I've found some types of moats that seem particularly robust:

Network effects: When the things become more valuable as more and more people use them. Take Microsoft Teams – the more people who use it, the more valuable it becomes for everyone.

Switching costs: When it's an actual hassle for customers to switch to a competitor. Once a whole operation of a company is running on Microsoft's cloud services, it would be extremely disruptive to change providers.

Brand power: When customers willingly pay a premium to a favorite product.

Scale advantages: When size translates to cost advantages that no smaller competitor can replicate.

I'm getting better at being able to tell when a moat is strengthening versus when it's weakening. I've found that looking at gross margins over time can be incredibly revealing – are they flat or improving? That's typically a pretty good sign that a company's competitive moat is still in place.

Characteristic #2: Capital-Efficient

The second characteristic that's really stood out in my research is capital efficiency – basically, how much a company needs to invest to generate growth.

I used to think growth was growth, regardless of how it was achieved. But I've learned that's not the case at all.

Some companies need to pour tons of money into new factories, stores, or equipment just to grow a little bit. Others can grow substantially while investing much less.

I've become particularly interested in Return on Invested Capital (ROIC) as a way to measure this. Companies that can generate high returns on the capital they invest create a much more powerful compounding machine.

Amazon is fascinating in this regard:

Their ROIC has grown from around 5% to 17% as they've matured. This shows that all those years of heavy investment are now paying off – for every dollar Amazon invests today, they generate significantly more in returns than they did a decade ago.

I've been especially drawn to businesses with high operating leverage. These are companies where once they've covered their fixed costs, a large percentage of each additional dollar of revenue falls to the bottom line as profit.

Software companies like Microsoft demonstrate this beautifully. After they've built their product, each additional customer comes with very low incremental costs but nearly the same revenue. As they grow, they become more profitable, not less.

This is so different from many traditional businesses where growth often leads to margin compression as companies move beyond their core markets.

Characteristic #3: Pricing Power Through Economic Cycles

The third characteristic I've found crucial is pricing power – a company's ability to raise prices without losing customers.

This one really hit home for me during our recent inflation spike. Some businesses had to absorb higher costs and saw their margins squeezed. Others were able to pass those costs on to customers and maintain or even expand their margins.

Google (Alphabet) shows remarkable pricing power in its advertising business. Despite new platforms constantly emerging, advertisers continue to pay premium prices for Google's ad inventory because the return on investment is so compelling.

I've noticed that companies with genuine pricing power often share a few traits:

They provide something that the customer actually needs or desires greatly

Their product or service is a low percentage of the customer's total expenditure

There are no decent substitutes

Pricing power isn't just about raising prices – it's about creating so much value that customers willingly pay more over time without jumping ship.

I've started to pay attention to how companies behave during a downturn. Do they have to slash prices to maintain volume? Or can they hold firm? The latter is generally a sign of a company with real staying power.

Trait #4: Long-Term Visionary Management

The fourth quality I've come to think is essential: excellent management with genuine long-term vision.

Over a ten-plus year holding period, there will be innumerable challenges and opportunities that nobody can anticipate today. Management's ability to respond to these changes while staying focused on long-term value creation is critical.

I have been reading about Microsoft under Satya Nadella, and it was very enlightening. When he took over as CEO in 2014, Microsoft was lagging in mobile and cloud computing. Rather than defend the Windows-centric model that had made Microsoft wealthy, Nadella made a bold move and adopted cloud-first, mobile-first, and even hug other platforms such as iOS and Android

This long-term plan required short-term sacrifices but positioned Microsoft ideally for the age of cloud computing. Azure is now driving Microsoft's growth.

I'm still developing my skill at evaluating management teams, but I've seen several indicators that seem to be pointing to exceptional leadership:

They invest billions in the future even when Wall Street is screaming for short-term gains

They're transparent about challenges rather than only boasting about wins

They wisely deploy capital into growth investments, smart acquisitions, and shareholder returns

I've also learned to watch out for red flags: excessive compensation packages, empire-building acquisitions, and prioritizing short-term earnings beats over long-term investments.

As shareholders, we're essentially hiring management to run our businesses. I want leaders who think like owners, not employees.

Characteristic #5: Businesses That Get Stronger With Scale

The fifth characteristic that's fascinated me is companies that actually get stronger, not weaker, as they grow larger.

Most businesses follow a predictable path – they grow quickly when small, but that growth inevitably slows as they saturate their markets and face increasing competition.

But there are rare businesses that create virtuous cycles where growth actually reinforces their competitive position.

Amazon exemplifies this perfectly. As they add more Prime members, they can spread fixed costs across more customers, enabling lower prices. Lower prices attract more customers, which gives them more scale to negotiate better rates with suppliers and more data to optimize their operations. This in turn allows them to offer even better selection and service, attracting yet more customers.

This isn't just linear growth – it's a compounding flywheel effect.

I've come to appreciate the enormous difference between linear and exponential advantages over decades. Linear advantages (like simply having more stores) can be replicated by competitors with enough capital. Exponential advantages (like network effects) become nearly impossible to disrupt once they reach critical mass.

I'm trying to identify these virtuous cycles by looking for companies where:

Their unit economics improve as they scale

Their moats widen rather than narrow over time

Data or network advantages compound with user growth

They become platforms that others build upon

These are the businesses where patience is most rewarded – every year you hold them, they're becoming structurally more valuable.

Building My "Forever" Portfolio

As I've learned about these characteristics of decade-long compounders, I've started reshaping how I think about my own portfolio.

Instead of asking "What might go up next month?" I'm trying to ask "What businesses have such extraordinary economics that I'd be happy to own them for the next 20 years?"

I've started keeping a watchlist of excellent businesses and trying to be patient, waiting for temporary market dislocations to buy them. The market regularly offers opportunities to buy great companies at reasonable prices during corrections or when they face short-term challenges.

I'm also working on my psychological framework as an investor:

Focusing on business performance, not daily stock price movements

Using market volatility as an opportunity, not a threat

Tuning out the noise of financial news and social media

Building conviction through deep understanding

I'm still figuring out when it makes sense to sell a long-term compounder. So far, I've concluded it should be pretty rare, but there are legitimate reasons:

When my original investment thesis is broken (not just delayed)

When the competitive landscape fundamentally changes

When I find a significantly better opportunity elsewhere

I've come to believe that truly exceptional businesses are relatively rare – perhaps just 25-50 companies globally at any given time. I'd sooner have a focused list of these compounders than be watered down by lower-quality businesses.

What I've Learned About Patience

The five characteristics we've explored – durable moats, capital-efficient growth engines, pricing power, exceptional management, and businesses that strengthen with scale – have become my framework for identifying companies worth holding for decades.

Finding companies with all five of these characteristics is not easy, but I'm sure the reward for doing so and then simply waiting patiently is tremendous.

While most of the investors I know are obsessed with quarterly reports and near-term stock price activity, I'm trying to build wealth via the alchemy of compounding over time.

I'm still a novice at the game of investing, and I'm aware that I have lots to learn. But one thing is certain to me: investing has nothing to do with being the smartest guy in the room.

It has everything to do with having the right temperament to let time do its wonders with wonderful businesses.

Most valuable riches are built not by trading in and out of shares but by owning fantastic businesses for nicely long times.

Look at your own portfolio. Which companies have these characteristics? Which ones are you confident enough to hold for the next decade or more?

Those are the questions I'm focusing on... and I think you should too.

Solid breakdown of what makes a true long-term compounder.

Temperament is key....ability to hold and wait when there is so much of news flow good and bad