Shopify's Blueprint: Growth, Innovation, and Resilience

A Breakdown of Q1 Performance, Strategic Initiatives, and Future Outlook

Shopify sees the bumpy road ahead.

They’re not blind to the wild world of global trade and talk of slowdowns. But looking at their own numbers through April, they just aren't seeing their merchants' sales (that's GMV, or Gross Merchandise Volume, for us layfolk) taking a nosedive.

Note I do not own Shopify - nor is this financial advice. This article explores what the talking points were in the most recent earnings call of May 2025

Shopify's pretty proud of how nimble they are, helping their sellers twist and turn with whatever the trade winds blow in – new tariffs, weird regulations, you name it, they’ve jumped on it fast.

Think about it: their sellers are all over the map, in every kind of business, big and small. No single type of merchant calls the shots, which gives them a solid footing.

And get this: for nearly a decade, 38 out of 39 groups of new merchants each quarter have actually grown faster than the whole e-commerce market. That’s a pretty solid track record of beating the odds.

Now, for their Q1 numbers.

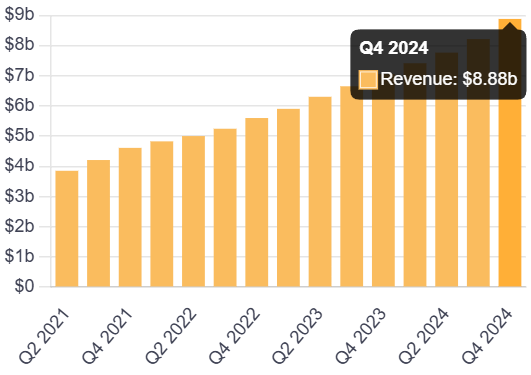

Revenue shot up 27% from last year.

They even pocketed a 15% free cash flow margin.

Their merchants sold a whopping $74.8 billion worth of stuff, a 23% jump. This was thanks to strong sales from existing stores, a bunch of new sellers signing up, and Europe really showing up.

Even their offline sales (think brick-and-mortar stores using Shopify) grew 23%.

Business-to-business sales went through the roof again with triple-digit growth.

International sales climbed 31%.

Shopify Payments is now used in 64% of transactions, partly because they rolled it out in 16 new countries.

Revenue from subscriptions was up 21%, and their big-shot Plus plan now makes up 34% of their monthly recurring cash.

Gross profit climbed 22%. The overall gross margin did dip a bit (49.5% down from 51.4%), but they say that’s because of a shift in what’s selling (more of the lower-margin payments), their expanded deal with PayPal, and losing some high-margin partnership money.

They kept a lid on operating expenses, spending $966 million, which is 41% of revenue, showing they’re still keeping an eye on costs.

So, what’s pushing their growth?

They’ve made big strides in helping merchants deal with the headaches of selling across borders.

They’ve got new tools live right now for figuring out duties at checkout, showing prices with duties already included, and even a new AI gizmo (TariffGuide.ai) to guess import duties.

They're also rolling out ways for sellers to prepay duties on shipping and expanding their fulfillment network so sellers have more local warehouse choices.

And their Shop App? It launched a “buy local” filter that got hundreds of thousands of people clicking.

They’re clearly moving fast, spitting out new features to deal with rule changes in days, sometimes even over a weekend.

Let’s talk payments.

Shopify Payments is now live and kicking in 39 countries – that’s almost double the 23 they had at the end of 2024.

Just recently, they launched multi-currency payouts for 20 European countries.

And Shop Pay? It handled over $22 billion in sales in the first quarter alone.

More big companies are jumping on board, adding Shopify’s payment and checkout systems – think Coach, Kate Spade, Purple, and Birkenstock.

AI is a big deal for them now. It’s at the heart of how they run their own business and how they build new stuff. They’ve basically told their teams to try AI first before asking for more people.

Internal AI tools, like some new MCP servers they built, are making their own work smoother. For merchants, they’ve revamped their AI assistant, Sidekick, making it smarter and better with languages; the number of merchants using it every month has more than doubled since the year started.

They also snapped up a company called Vantage Discovery back in March 2025 and are using its tech to beef up "AI-powered multivector search" on storefronts.

Globally, Europe is on fire for them, with sales growing 36% in Q1, especially in the UK, Netherlands, and Germany. They’re getting better at tailoring things for local markets (like AI-powered translations and making sure they’re following privacy rules) and their marketing is helping them get a bigger slice of the international pie.

They’ve also got their eyes on Latin America and Asia as the next big places to grow.

And it's not just small online shops. Big retailers and mid-sized businesses, both online and offline, are really getting into Shopify.

They recently signed up VF Corp (who own brands like JanSport and Dickies), Follett Higher Education (with over a thousand college bookstores), and Caring Beauty (a luxury fashion group), among others.

Their offline business, the point-of-sale stuff, is something they’re planning to grow for years. They say their speed in rolling out products and their ability to connect online and offline sales give them an edge over the old-school providers.

New features like same-day delivery through Uber/DoorDash, tap-to-pay, and shipping to stores are getting those large, complicated retailers with multiple locations to sign up.

Now, about those gross margins. The margin on Subscription Solutions is holding steady around 80%. The margin on merchant solutions is lower and has been squeezed by more payment processing (which has lower margins), changes in how they account for PayPal, and the types of merchants signing up.

They expect the hit to margins from expanding payments into new countries and attracting more big merchants to be temporary. These should even out as their other high-margin products pick up steam.

They do see some temporary slowdowns for subscription growth in 2025 because of longer paid trials and the last bits of their Plus plan pricing changes.

Liking this post? Please share with a friend - Help expand the growth of retail investors.

How are they getting new customers? Their marketing is all about performance. They’re flexible with their budget, shifting it based on what’s bringing in returns now and what looks like a good long-term bet.

No big changes to their overall marketing plan; they’re spending to support both their usual markets and new growth areas, and it covers all types of sellers. Because they watch the data like hawks, they can see super fast if their cost to get a customer (CAC) or the lifetime value (LTV) of that customer changes, letting them switch things up quickly.

What’s the outlook?

For Q2, they’re expecting revenue to grow in the “mid-twenties” percent range, even with all the trade drama, and a little help from favorable currency exchange rates.

They think Q2 gross profit dollars will grow in the high teens, though the margin mix will shift a bit with more payment activity.

Operating expenses for Q2 should be around 39-40% of revenue, which is better leverage than last year.

And they expect that free cash flow margin to stay in the mid-teens.

Management is clear: they’re focused on investing in products and growth rather than trying to squeeze out extra margin points right now.

What about all those tariffs and trade issues? Shopify has been quick to build tools and features to help merchants deal with new tariffs and rule changes. So far, only about 1% of their merchants' sales are tied to imports from China that used to get a tax break (the de minimis exemption), so the direct hit from tariffs is pretty small. Most of their cross-border sales are between the US and Europe.

Merchants are getting creative to handle supply chain problems – they’re not just raising prices. They’re finding new suppliers, changing up the products they sell, and tweaking when they order inventory.

Plus, Shopify buyers in the US tend to have higher incomes, which might mean they’re not as freaked out by price increases from tariffs or inflation.

And all this new AI agent stuff, fancy LLM-powered search, and weird new ways people find products? Shopify sees these as big chances, not threats. They’re investing in partnerships and linking up with the big AI platforms to make sure their merchants’ products show up wherever people are looking and shopping.

They think expanding into these new areas will just make Shopify even more valuable to their sellers.

At the end of the day, their whole philosophy is “merchant first.” They build products and run their company with that in mind.

They’ve set themselves up to be flexible, react fast, and, as they put it, “shoulder complexity” for their merchants.

They’re playing the long game, focusing on steady growth, new ideas, running efficiently, and giving their merchants real value, no matter what the economy is doing.

Valuation and Future Projections

Shopify is a harder company to predict for the next 5 years simply because they are in a rapid growth phase.

When companies are expected to grow their earnings per share by 20+% it usually commands a higher P/E ratio. However as the company matures the P/E should slowly overtime go to a normal rate. Here is the P/E the last 3 months (trending down):

When it comes to Shopify, their current P/E is 60 (TTM). The stock is at $94. If we assume 20% EPS growth (on average for the next 5 years), and a terminal P/E ratio of 45, you receive annualized returns of 13% year over year at the current price.

This sounds great but it is commanding a lot out of the company.

Say headwinds approach Shopify in the future and their P/E goes to 35 (still more expensive than a company like Amazon) and they still manage to grow their EPS by 15% year over year: This will get you only 3% annualized returns year over year.

In my opinion, the stock is premium priced. It is a great company and I would love to own it but not at the current price.

For the expectations and what needs to happen (and as a long term investor) I believe putting money in a S&P 500 index fund will be more predictable and offer solid returns over the cost of investing in Shopify.